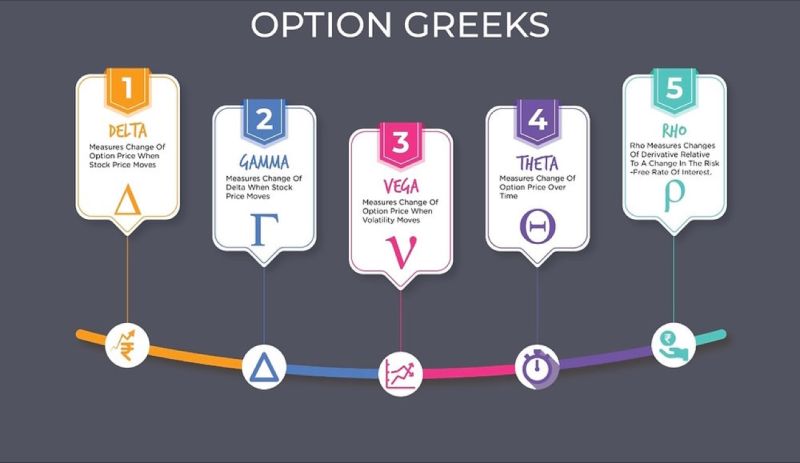

11. What is the formula of Delta for call and put option?

The formula for calculating the delta of a call option and a put option is as follows:

1. Delta for Call Option (Δc):

Δc = N(d1)

Where:

· Δc = Delta for the call option.

· N() = The cumulative standard normal distribution function.

· d1 = The formula for d1 is given by: d1 = (ln(S/K) + (r + (σ^2)/2) * T) / (σ * √T)

Where:

· S = Current price of the underlying asset.

· K = Strike price of the option.

· r = Risk-free interest rate.

· σ = Volatility of the underlying asset’s returns.

· T = Time to expiration of the option in years.

2. Delta for Put Option (Δp):

Δp = N(d1) – 1

Where:

· Δp = Delta for the put option.

· N() = The cumulative standard normal distribution function.

· d1 is the same as defined for the call option above.

These formulas provide the delta value for call and put options. Delta measures the sensitivity of the option’s price to changes in the price of the underlying asset. A positive delta for a call option indicates that its price increases as the underlying asset’s price rises, while a negative delta for a put option indicates that its price increases as the underlying asset’s price falls.

12. Can you draw the graph of delta of call and put option?

15. What are the implications of Put Call Parity on Delta?

Put-Call Parity is a fundamental concept in options pricing that relates the prices of European call and put options with the same strike price and expiration date to the price of the underlying asset. It has important implications for understanding the relationships between the delta of call and put options and how they can change as market conditions or option parameters change.

Here are the key implications of Put-Call Parity on delta:

Put-Call Parity implies that the delta of a European call option minus the delta of the corresponding European put option is equal to 1. In other words:

Δc – Δp = 1

This relationship holds as long as the options are European-style, have the same strike price, and the same expiration date.

Where:

- Δc is the delta of the call option.

- Δp is the delta of the put option.

21. Can you draw the graph of gamma for an option?

The best way to understand the graph of gamma, is to take the graph of delta and differentiate it point-wise. We take the delta graph (red), find the tangent at each point (blue line), whose slope gives us the value of gamma (blue circle), which we then connect up to get the gamma curve (yellow).

22. What are the implications of put call parity on Gamma?

Put-call parity is a fundamental concept in options pricing that establishes a relationship between the prices of European call and put options with the same strike price and expiration date.

After differentiating the put call parity formula with respect to underlying, we can get the following formula:

Let’s differentiate this with respect to the underlying, and we obtain:

γc – γp = 0

γc = γp

As such, when we talk about the gamma of an option, we often do not need to specify whether it’s the put or the call. We can consider either scenario, and it often easier to consider call options which have a positive delta.

27. How does theta behave when option reaches maturity?

As expiration gets closer, the time value of an options contract decreases. Before expiration, the time value of an option is at least 0. The longer the time until an options contract expires, the greater the opportunity for the underlying security’s price to move and increase its intrinsic value, so the contract has more time value. Basically, with more time on the clock, more price movement can happen.

Time decay, theta burn, and theta decay are synonymous and refer to the decline in the value of an options contract as expiration approaches. Time decay is non-linear, meaning the rate of change increases as the options contract approaches expiration.

The time value of an options contract decreases at an accelerating rate as expiration approaches. For example, time decay increases more rapidly from 60 to 30 days than from 90 to 60 days. While an option’s time value decreases over time, other extrinsic factors, like implied volatility, may increase as expiration approaches, offsetting or exceeding theta decay. Still, it is important to know options are decaying assets and lose time value daily.

36. How maturity affects Vega?

Maturity, or the time to expiration, can have a significant effect on Vega, the sensitivity of an option’s price to changes in implied volatility. The relationship between maturity and Vega is as follows:

Longer Maturity Options Have Higher Vega: Options with longer time to expiration tend to have higher Vega values. This means that their prices are more sensitive to changes in implied volatility compared to options with shorter maturities.

For example, if you compare two otherwise identical call options, one with an expiration of one year and the other with an expiration of one month, the one-year option is likely to have a higher Vega because it has more time for implied volatility to potentially change.

Shorter Maturity Options Have Lower Vega: Conversely, options with shorter time to expiration tend to have lower Vega values. This means that their prices are less sensitive to changes in implied volatility compared to options with longer maturities. Continuing with the example, the one-month option is likely to have a lower Vega compared to the one-year option because there is less time for implied volatility to have a significant impact.

37. When is Vega highest?

Vega is typically highest for at-the-money (ATM) options that have longer times to expiration.

Longer Time to Expiration: Options with longer times to expiration generally have higher Vega values. This is because options with more time until expiration have more time value, and therefore, changes in implied volatility have a larger impact on their prices. ATM options with longer expirations, are more sensitive to changes in implied volatility because there is more time for potential price movements in the underlying asset to occur.

Vega Tends to Peak at ATM: Vega is not constant across all strike prices and maturities. It often peaks for ATM options with longer maturities because these options have the most time value and are highly sensitive to changes in implied volatility.

40. What are the implications of Put-Call Parity on Vega?

This tells us that the vega of the call and the put on the same strike and expiration is the same. Thus, to know the vega of an option on a strike, we can consider either the call or the put option.