Financial Engineering Interview Questions (50 Q&A)

Fixed Income: Mortgage Backed Securities (27 Q&A)

Time Series Analysis (30 Q&A)

Linear Regression (24 Q&A)

Options and Derivatives (50 Q&A)

Options and Derivatives (43 Q&A)

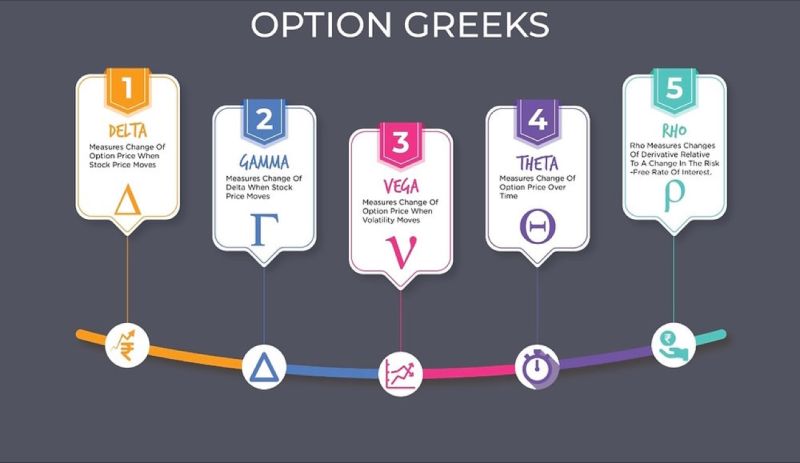

Greeks Option Pricing (50 Q&A)

Geometric Brownian Motion (9 Q&A)

Portfolio Theory (22 Q&A)

Fixed Income Products & Risk Management (45 Q&A)

Black Scholes Model (7 Q&A)

Monte Carlo - Risk & Option Pricing (22 Q&A)

Python Interview Guide (90 Q&A)

"Options, Futures, and Other Derivatives" - John C. Hull

"Bond Markets, Analysis, and Strategies" - Frank J. Fabozzi

"Market Risk Analysis: Practical Financial Econometrics" - Carol Alexander

"Risk Management and Financial Institution" - John C. Hull

"Market Risk Analysis: Quantitative Methods in Finance" - Carol Alexander

"Advances in Financial Machine Learning" - Marcos Lopez De Prado

"A Primer for Mathematics of Financial Engineering" - Dan Stefanica

"Monte Carlo Methods in Financial Engineering" - Paul Glasserman